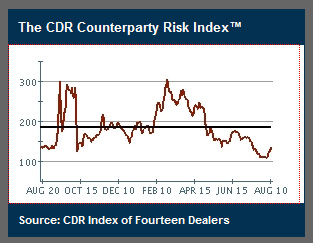

After August 2009, you can mentally add the current chart to the rightmost part of the above .

This page is part of the homeplace advertisement-free web portal.

"best indicator for the NEXT financial implosion.” Covers real banks plus INVESTMENT 'bank's."

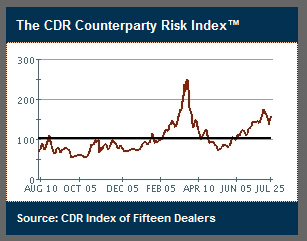

CDR's Counterparty Risk index fluctuates over time but normally would be between 10 and 15 basis points (0.1% to 0.5%). The March 2008 Bear Stearns implosion high was 250 (2.5 %) in March 2008. BIG is BAD! As of June 2008 the index is over 100 and rising!!

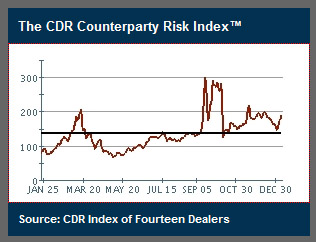

The Counterparty Risk Index can be seen from these 3 overlapping charts ending on July 29, 2008, January 15, 2009, and on Aug 18, 2009:

After August 2009, you can mentally add the

current chart to the rightmost part of the above .

Note the sudden doubling in mid March 2008. This is the Bear Stearns Implosion.

Note the sudden doubling in September 2008. This is when Lehman went bust (filed for bankruptcy Sept. 15) and AIG had to be bailed out (late Sept.).

Notice that the brief stock market honeymoon starting mid-December 2008 and the rocky first 2 weeks of January 2009 are foreshadowed by this [counterparty] risk index.

Wednesday Jun 18 2008

All times are London time

Counterparty

risk is all the rage in this post Bear Stearns world, and Credit

Derivatives Research is hoping jittery investors will take a shine

to its latest product - an index designed to track the credit risk

of those banks and brokers who are the counterparties to most of the

contracts traded in the CDS market.

Counterparty

risk is all the rage in this post Bear Stearns world, and Credit

Derivatives Research is hoping jittery investors will take a shine

to its latest product - an index designed to track the credit risk

of those banks and brokers who are the counterparties to most of the

contracts traded in the CDS market.

The index averages the market spreads of the credit default swaps of the 15 major credit derivatives dealers -

ABN Amro,

Bank of America,

BNP Paribas,

Barclays,

Citigroup,

Credit Suisse,

Deutsche,

Goldman,

HSBC,

Lehman,

JP Morgan,

Merrill,

Morgan Stanley,

UBS, and

Wachovia.

CDR’s chief strategist, Tim Backshall, says the group intends to license the index for trading either on an exchange or over-the-counter, so that investors “have a medium for laying off counterparty risk in a general way” - as opposed to buying CDS on an individual basis.

What is more interesting at this point is what the CDR Counterparty Risk index shows. As of June 13, the index was hovering around 118.7bp - in line with its year-to-date average of 116.9 and well below its Bear Stearns-induced peak of 250. In other words, traders in the CDS market seem to the think the crisis in financials is past (Lehman Brothers notwithstanding), although the market is a long way from those heady days when banks and brokers traded at 10 or 11bp.

June 17, 2008, 12:37 pm

Measuring Credit Risk in Financial Stocks

Posted by David Gaffen

How do investors view the financial-services companies? Serena Ng has this report on one new index tracking the cost of insuring that they don’t default.

Over the past year, the market has come to view prices of credit default swaps tied to Wall Street firms and other major financial institutions as a key indicator of investor concern about the health of these firms.

A new index of credit default swaps aims to track this more closely, and it is signaling that some strains are still present.

The CDR Counterparty Risk Index, created by Credit Derivatives Research in Walnut Creek, Calif., is made up of credit default swaps tied to 15 major financial institutions, including Citigroup, Merrill Lynch, Morgan Stanley, Lehman Brothers and Deutsche Bank.

In a credit default swap, one party buys protection on a specific bond from another party, which in turn agrees to compensate it if the bond defaults. If more people want to buy protection, CDS “spreads” rise.

In March, spreads on CDS tied to Bear Stearns surged to over 750 basis points, or more than $750,000 annually to insure against a default in $10 million of Bear debt over five years. At the time, many firms that had outstanding trades with Bear purchased credit protection on Bear itself because they were nervous about the firm’s ability to meet its trading obligations.

The CDR Counterparty Risk Index, which averages the CDS spreads of its components, peaked at around 250 basis points during the Bear crisis. It is now at around 100, though that’s still twice as high as its level in October 2007, and it has been edging higher in recent weeks.

Many traders and analysts currently use another derivative index, the Markit CDX, to trade and gauge credit risk of financial firms and other investment-grade credits. But the CDX doesn’t include swaps that reference the Wall Street investment banks and major dealers. That’s partly because the CDX is created and traded by many of these same banks, and trading the index involves taking positions in all the swaps that comprise it.

Permalink | Trackback URL: http://blogs.wsj.com/marketbeat/2008/06/17/measuring-credit-risk-in-financial-stocks/trackback/